Cheaper Isn't the Whole Story. The Map Is.

Where Chinese specialty grades match Western on specification and qualification today, where they're narrowing, and where Western specialty grades still hold — across the four engineering polymers in active compression: PA6, PA66, PBT, POM.

Part 1 (PA66 Isn't a One-Off. It's a Cycle.) laid out the cycle: chemistry bottleneck breaks, Chinese capacity outpaces domestic demand, exports flood, commodity prices collapse, Western specialty-grade premium compresses through buyer leverage on a four-to-five-year lag. Eight polymers climb that ladder on staggered clocks. PC is in late-stage compression; PA12, LCP, industrial PEEK, and PA10T are just starting. Four sit in active compression today — PA6, PA66, PBT, POM — with PA6's already-played-out arc as the empirical precedent for the other three.

This piece is the operational read on those four — where each application sits today, and what the buyer can act on in 2026. Chinese specialty grades are cheaper. Cheaper alone isn't the right choice on every program: process consistency, batch quality, and service-history gaps carry real risk on long-life programs, where a single field failure erases years of price savings. The picture differs by polymer — each clock set by when its bottleneck broke — and by application: heat resistance, hydrolysis, flame retardance, and fatigue each run their own substitution clocks.

Where each polymer sits today

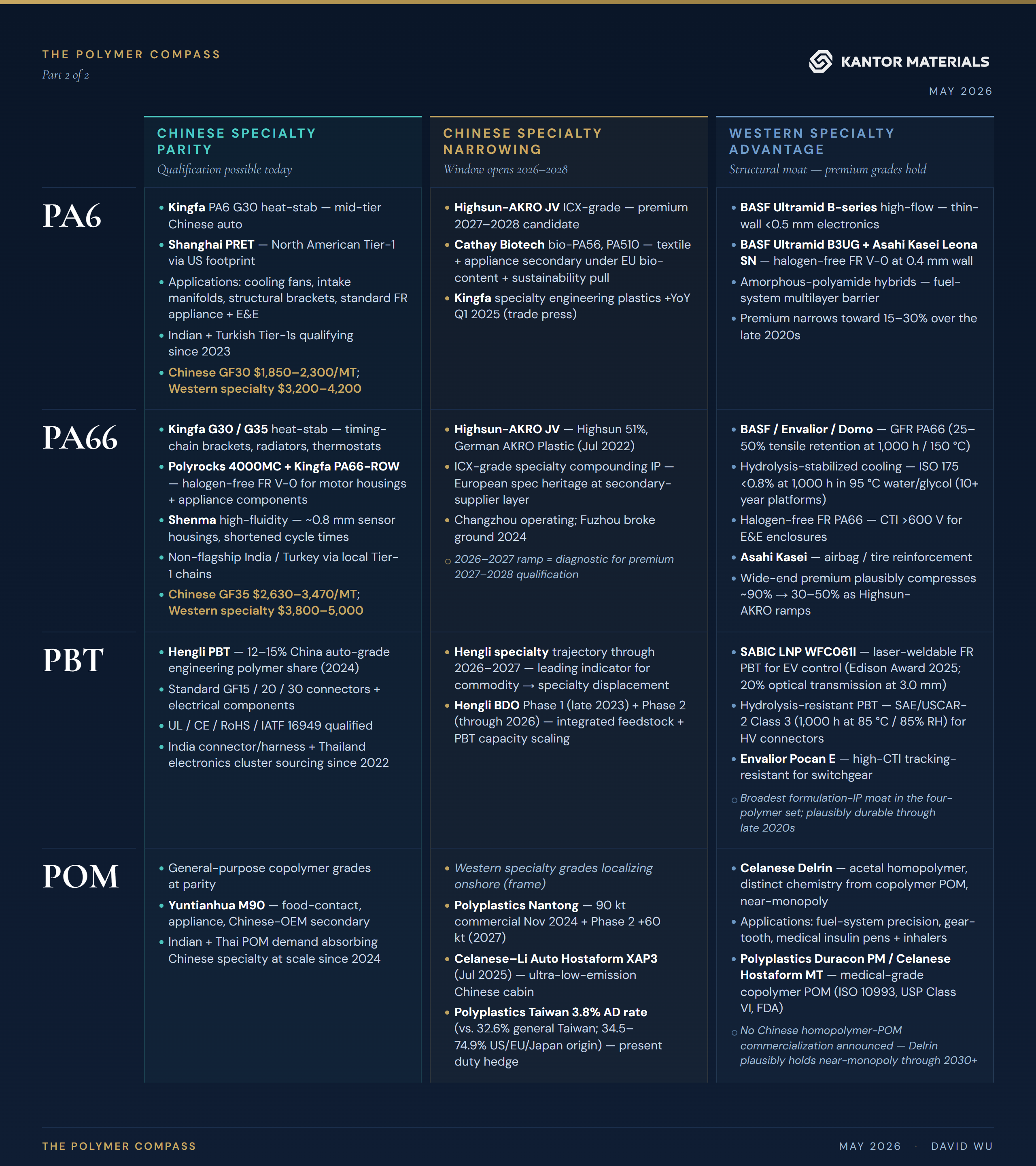

The four polymers in active compression, mapped across three states: where Chinese specialty grades match Western on spec and qualification, where they're closing the remaining gap, and where Western specialty grades still hold.

Full grade-by-grade detail with spec thresholds, application enumeration, and named-OEM and regional qualification context is in Appendix Table 1 at the bottom of this article.

Two dynamics shaping 2026

The 2026 action concentrates on PA66 (mid-compression, the most active polymer in the set) and POM (Western incumbents localizing onshore). PA6 and PBT are quieter this year — PA6 mostly settled-cycle, PBT not yet to act on. The polymer-set's structural extremes — Delrin's durable moat, Cathay's bio destination — anchor the close.

On PA66, Chinese GF35 prices $2,630-3,470/MT (April 2026) sit against Western specialty automotive PA66 at $3,800-5,000 — a premium ranging from roughly 10% at the narrowest grade-on-grade comparison to ~90% at the widest. The wide end plausibly compresses toward 30-50% as the Highsun-AKRO ramp matures. Watch the 2026-2027 plant ramp: if German specialty discipline transfers cleanly through the JV structure — carrying AKRO's spec heritage into Chinese production — premium Western automaker programs become qualification candidates in 2027-2028. Ascend's wind-down separately redistributes several hundred thousand tons of supply; Chinese specialty grades can absorb that volume as the wind-down completes, on non-safety-critical applications first.

POM has Western incumbents localizing onshore. Two signals: Polyplastics' 90 kt Nantong plant began commercial production in November 2024 (Phase 2 +60 kt scheduled 2027), and Celanese launched the Li Auto co-branded Hostaform XAP3 in July 2025. Nantong was conceived as a market-localization play before China's May 2025 antidumping duties on imported copolymer POM; the AD wall validated the decision rather than triggering it. The XAP3 launch is consistent with two non-exclusive mechanisms — defensive positioning against maturing Chinese qualification, and the value of a premium customer relationship in a fast-growing EV segment. The observable signal across both Nantong and XAP3: Western formulation IP moving onshore on Chinese OEM programs.

At the four-polymer set's structural extremes, no Chinese homopolymer-POM commercialization is announced — Delrin's integrated formaldehyde-purification and end-capping process is the most durable patented-chemistry moat in the set, plausibly holding near-monopoly through 2030 and likely beyond. On the bio side, Cathay Biotech's PA56 and PA510 (glucose-derived pentamethylene diamine, with PA510's sebacic from castor oil) have no named-OEM qualification in the public record; the credible near-term path runs through automotive interior textile and appliance secondary structure under EU bio-content and sustainability mandates.

Why the moats hold (and which fall first)

Four moats, four mechanisms, four timelines.

Process consistency — distillation purity, gel control, multi-year statistical process capability — falls fastest as Chinese producers accumulate operating hours. Expect Western premium compression within 24-36 months of each polymer's commodity-tier break. PA6 closed broadly by 2024-2025; PA66 is closing now; PBT closes 2027-2029; POM is slowest, gated by the trioxane learning curve.

Formulation IP — the validated multi-additive packages behind heat-stabilized PA66 GFR, halogen-free FR PA66 for E&E, and hydrolysis-stabilized PA66 cooling — erodes through cycles of OEM-feedback iteration. Chinese compounders can buy the additives separately but cannot reconstruct validated combinations and loadings without years of tuning. Partial compression within five years of commodity break; the most additive-heavy premium grades hold past 2030.

Service history and certification closes only as years of supply accumulate: medical audit trails, automotive PPAP on a specific platform, multi-year field-failure data. A Chinese producer can match the polymer and the additive package on paper, but without service history on the specific platform-grade combination, the OEM won't approve the swap. This moat cannot be cloned faster than time itself.

Patented chemistry and integrated process know-how is the slowest. Delrin homopolymer's integrated formaldehyde-purification, anionic-polymerization, and end-capping process runs as trade-secret know-how — foundational patents expired decades ago, but no Chinese producer has commercialized homopolymer POM at scale. Specific premium PPA grades (DuPont/Celanese Zytel HTN-class) and patent-protected halogen-free FR additives sit alongside. These positions hold on a five-to-ten-year horizon, until integrated processes are replicated or alternative chemistries emerge.

The order shapes how Chinese specialty grades enter the chain: process closing earns mid-tier qualification; formulation IP opens premium grades; service history catches up only with time; patented chemistry holds independent of qualification work.

There's a fifth dynamic above the four moats. Western specialty grades don't compress to extinction — they migrate upward into chemistries the four-polymer sequence doesn't reach. PPA (BASF Ultramid Advanced N, Solvay Amodel, DuPont Zytel HTN, Kuraray Genestar) and PA46 (Envalior Stanyl) are the destination. Chinese producers sit roughly five years behind Western on most PPA chemistries (PA10T is the partial exception); spec premiums on PPA run 1.5-3× over engineering-grade PA66 depending on the chemistry within the family. Global PPA production was ~176,000 tons in 2024 (under 10% the size of PBT), but value-per-ton anchors Western specialty profitability through the late 2020s. For mid-tier distributors and component suppliers in Global South markets, PPA isn't yet a substitution play — Chinese capability is too far behind, and the volumes too small relative to PA66 and PBT to anchor commercial focus. PPA matters as the structural context for why Western specialty doesn't disappear — it shifts.

The AVL inversion as the binding constraint

Each polymer's commodity break is followed, on a four-to-five-year lag (the PA6 empirical window, with polymer-specific variation), by a specialty-grade compression that runs until approved-supplier-list (AVL) inertia becomes the binding constraint. The question then shifts from "can Chinese specialty grades qualify?" to "will the buyer invest re-qualification work on programs that are themselves winding down?"

The current Western specialty-grade moat — formulation IP, process control, certification accumulation, buyer-validated additive combinations — protects through AVL inertia. Automakers and electronics brands add suppliers slowly and remove them slowly; AVL entries on legacy combustion-engine platforms persist through the platform's full life (8-12 years) absent a specific trigger. That inertia is the structural moat through 2028-2030.

After 2030, the inertia plausibly inverts. As ICE platforms wind down across European, Chinese, and increasingly North American markets, buyers face two paths: maintain qualified Western suppliers across shrinking ICE volumes (paying premium on declining production), or accept Chinese specialty grades on programs winding down anyway. The second is the path of least resistance when re-qualification cost is small relative to remaining program savings — but it isn't the only path. The directional pressure inverts; the timeline depends on how each OEM weighs re-qualification cost against residual ICE program economics.

Three factors could delay the inversion past 2030: (1) ICE platform extension if EV transition slows under recession or fuel-price relief, stretching combustion runs and keeping AVL inertia alive; (2) premium-tier formulation IP (heat-stabilized PA66 GFR, halogen-free FR PA66 above CTI 600V, hydrolysis-resistant PBT for HV connectors) proving more durable than the maturation curve suggests; (3) OEM lock-in from the 2021-2024 PA66 price spike — buyers who re-qualified PBT or PA6 during that spike won't re-qualify back to PA66, even at materially lower Chinese specialty-grade prices, without a multi-year stable price signal. The directional inversion holds; the timing is uncertain.

The AVL inversion has been playing out on PA6 across 2022-2026 — what remains is what the formulation-IP and patented-chemistry moats genuinely defend. PA66's inversion plausibly reaches the same equilibrium on a comparable lag from the ADN break, with polymer-specific qualification cycles widening the range; PBT's follows BDO on a similar window; POM is the slowest, gated by the trioxane learning curve.

What this framework doesn't claim

The thesis: Chinese capacity at scale produces commodity-to-specialty-grade compression on a staggered clock across the four polymers, with AVL inertia as the binding constraint on Tier-1 programs through 2028-2030. What it does not claim: that the inversion is monotonic, that the order is invariant by region, or that Western specialty grades necessarily lose pricing power in absolute terms. Several pressures could reverse the directional read. Geopolitical de-risking — US Section 301 expansion, EU CBAM Phase 2 from 2026, India safeguard duties — could lock global Tier-1 OEMs into Western specialty supply on ICE sunset platforms precisely because Chinese-origin chemistries become a supply-chain liability. Western specialty producers could price-cut to retain Tier-1 share, compressing margins instead of volumes. Hengli could stay in commodity tier (the historical pattern for large integrated producers), making specialty-focused compounders the leading indicator. And PBT and POM compressions may not follow PA6/PA66 cleanly — different chemistries, different bottlenecks, different formulation-IP depth. The mechanism is structural; the timing is contingent.

2026 qualification priorities

Priority order for qualification work this year:

PA66 first. Biggest opportunity, widest price gap, fastest moving. Ascend's bankruptcy redistributed supply across BASF (post-Solvay), Asahi Kasei, Invista, and the rising Chinese specialty-grade layer; Korean and European mid-tier automakers will plausibly accept Chinese specialty-grade PA66 fastest between 2026 and 2028. Once approved, the price savings run for the program's remaining life — typically 5-8 years for electronics and appliances, 8-10 for legacy auto platforms — barring a price action, supply disruption, or qualification challenge.

PA6 second. Most mature substitution path. Multiple Chinese specialty-grade PA6 products are already approved for mid-tier auto. Next step: higher-stability applications — heat-stabilized for hot engine bay, glass-reinforced for structural brackets, FR for EV battery housings. A single major auto program runs thousands of tons of PA6 per year; even partial capture of the price gap delivers material savings.

PBT next. Preparing for 2027-2028. Hengli's commodity-grade PBT capacity is scaling. Specialty-grade PBT — laser-weldable, FR, glass-reinforced for HV connectors and EV applications — follows on a longer cycle. Hengli's specialty trajectory through 2026-2027 is the leading indicator.

POM last. Hold-and-watch. Western specialty grades (Celanese, Polyplastics, BASF, Mitsubishi EP, LG Chem) retain ~70% of the global market through structural protection. Polyplastics' Nantong localization is the canonical Western onshore response, alongside the alternative pattern of Western producers ceding commodity tier and migrating up to PPA/PA46. Real substitution openings on premium applications are unlikely in this five-year window.

Per-application breakdown across under-hood and structural auto, precision injection, connectors and E&E enclosures, industrial FR enclosures, food-contact/appliance, and EV-specific categories is in Appendix Table 2 at the bottom of this article.

The dynamics above describe where AVL inertia is strongest: global Tier-1 OEM programs, premium-tier specialty grades, multi-year qualification cycles. Mid-tier regional automakers across India, Turkey, Vietnam, Thailand, and Indonesia, plus the Tier-1 ecosystems feeding them, run shorter cycles with less list rigidity; Chinese specialty grades have been qualifying into those buyers in real time, and the inversion thesis is less load-bearing where there was less inertia to invert. What translates is the price gap. When Western specialty-grade premium compresses on Tier-1 programs, it compresses across the chain. Distributors and traders who price-track Tier-1 movements have a meaningful lead — on the order of one to two pricing cycles — on what their regional buyers will demand.

Each engineering polymer's bottleneck breaks, commodity prices collapse, specialty premium compresses through buyer leverage, AVL inertia binds, then plausibly inverts as platforms wind down. The mechanism is invariant. The clocks are different. Qualification work gets done while the window is open, or later under tighter price gaps and shorter program tails. The map will keep moving. The window will not reopen.

← Part 1 (PA66 Isn't a One-Off. It's a Cycle.) for the full cycle and the PA6 precedent.

Appendix — Reference tables

Appendix Table 1 — Polymer maturation matrix

| Caught up — Chinese specialty grades match Western | Narrowing — closing the remaining gap | Western specialty grades still hold | |

|---|---|---|---|

| PA6 | • Mid-tier auto (cooling fans, intake manifolds, brackets, standard GF30) • Standard FR appliance + E&E enclosures • Chinese GF30 $1,850-2,300/MT (Apr 2026); Western specialty $3,200-4,200 • Indian + Turkish Tier-1s qualifying since 2023 | • Cathay bio-polyamides (PA56, PA510) under EU bio-content + sustainability pull on textile + appliance secondary • Specialty engineering compounding: Highsun-AKRO ICX, Kingfa specialty engineering plastics Q1 2025 +YoY (trade press) | • High-flow injection below 0.5 mm wall (BASF Ultramid B-series high-flow) • Halogen-free FR V-0 at 0.4 mm wall (BASF B3UG, Asahi Kasei Leona SN) • Amorphous-polyamide hybrids for fuel-system barrier • Premium plausibly narrows toward 15-30% over the late 2020s |

| PA66 | • Mid-tier under-hood on Chinese OEMs; non-flagship India/Turkey via local Tier-1 chains • Kingfa G30/G35 heat-stabilized: timing-chain brackets, radiators, thermostats • Halogen-free FR PA66 V-0 (Polyrocks 4000MC, Kingfa PA66-ROW) • Shenma high-fluidity for ~0.8 mm sensor housings • Chinese GF35 $2,630-3,470/MT (Apr 2026); Western specialty $3,800-5,000 | • Highsun-AKRO JV (Highsun 51%, German-owned AKRO Plastic; Jul 2022) • AKRO contributes ICX-grade specialty compounding IP with European specification heritage • Changzhou operating; Fuzhou broke ground 2024 • 2026-2027 ramp is the diagnostic — opens premium Western automaker qualification 2027-2028 if discipline transfers cleanly | • GFR PA66 under-hood: 25-50% tensile retention at 1,000 h/150°C (BASF, Envalior, Domo) • Hydrolysis-stabilized cooling: ISO 175 below 0.8% at 1,000 h in 95°C water/glycol • Halogen-free FR PA66 with CTI above 600V for E&E • Airbag + tire reinforcement (Asahi Kasei among leading Asia-based suppliers) • Wide-end premium plausibly compresses from ~90% toward 30-50% as Highsun-AKRO ramps |

| PBT | • Standard PBT GF15/20/30 for connectors + electrical components • Hengli PBT captured 12-15% of China's auto-grade engineering polymer market in 2024 (UL, CE, RoHS, IATF 16949) • India connector/harness + Thailand electronics cluster sourcing since 2022 | • Hengli's specialty-grade trajectory through 2026-2027 is the leading indicator for when commodity displacement extends into specialty | • Laser-weldable halogen-free FR PBT for EV control units (SABIC LNP Thermocomp WFC061I, 2025 Edison Award; 20% optical transmission at 3.0 mm) • Hydrolysis-resistant PBT for HV connectors (SAE/USCAR-2 Class 3, 1,000 h at 85°C/85% RH) • High-CTI tracking-resistant PBT for switchgear (Envalior Pocan E) • Multi-additive formulation IP — Western specialty-grade PBT plausibly durable through the late 2020s |

| POM | • General-purpose copolymer grades (Yunnan Yuntianhua M90 for food-contact, appliance, Chinese-OEM secondary) • Indian + Thai POM demand absorbing Chinese specialty at scale since 2024 | • Western specialty grades localizing onshore • Polyplastics Nantong 90 kt (Nov 2024 commercial); Phase 2 +60 kt (2027) • Celanese-Li Auto Hostaform XAP3 (Jul 2025) — ultra-low-emission POM for Chinese cabin • Polyplastics Taiwan 3.8% AD rate (vs. 32.6% general Taiwan; 34.5-74.9% US/EU/Japan origin) is the present duty hedge | • Acetal homopolymer (Celanese Delrin) — distinct chemistry from copolymer POM, Celanese near-monopoly • Applications: fuel-system precision, gear-tooth, medical insulin pens + inhalers • Medical-grade copolymer POM: ISO 10993, USP Class VI, FDA (Polyplastics Duracon PM, Celanese Hostaform MT) • Delrin plausibly retains near-monopoly through 2030 and likely beyond |

Appendix Table 2 — Chinese specialty grades vs. Western specialty grades, by application

| Application | Caught up — Chinese specialty grades | Still Western specialty grades |

|---|---|---|

| Under-hood and structural auto (radiators, thermostats, intake manifolds, brackets, cooling fans) | PA66 G30/G35 heat-stabilized (Kingfa) for timing-chain brackets, radiators, thermostats. PA6 G30 (Kingfa) at mid-tier Chinese auto programs. Shanghai PRET PA6 reaching North American Tier-1 auto programs via its US footprint. | Glass-reinforced PA66 with 25-50% retained tensile at 1,000 h/150°C for thermal cycling. Hydrolysis-stabilized PA66 for cooling-system end tanks (10+ year platforms). Amorphous-polyamide hybrids for fuel-system multilayer barrier. |

| Precision injection (sensor housings, thin-wall electronic components) | Shenma high-fluidity PA66 grades for thin-wall sensor housings (around 0.8 mm), with shortened cycle times relative to standard grades. | High-flow PA6 below 0.5 mm wall section. Halogen-free FR PA6 with V-0 rating at 0.4 mm. |

| Connectors and E&E enclosures | PBT GF15/20/30 for consumer electronics and standard automotive connectors (Hengli broadly qualified). | High-CTI tracking-resistant PBT for switchgear (Envalior Pocan E). Laser-weldable halogen-free FR PBT for EV control units (SABIC LNP Thermocomp WFC061I). Halogen-free FR PA66 with CTI above 600 V for premium E&E. |

| Industrial FR enclosures (motor housings, instrument shells, appliance FR components) | Halogen-free FR PA66 V-0 — Polyrocks 4000MC, Kingfa PA66-ROW broadly qualified at the secondary-supplier layer. | Premium FR specialty grades with higher CTI thresholds. |

| Food-contact, appliance, secondary-supplier auto parts | POM at general-purpose — Yuntianhua M90, Polyplastics Nantong (90 kt plant in commercial production since November 2024). | Medical-grade copolymer POM with ISO 10993, USP Class VI, FDA approvals (Polyplastics Duracon PM, Celanese Hostaform MT). Delrin homopolymer for fuel-system precision parts and medical insulin pens/inhalers. |

| EV-specific (battery housings, high-voltage connectors, control units, cabin) | PA66 V-0 enclosures already qualified (Polyrocks 4000MC, Kingfa PA66-ROW). Chinese OEM-led EV programs increasingly prefer Chinese specialty grades. Celanese-Li Auto Hostaform XAP3 cabin POM launch (July 2025) is the canonical Western localization signal. | High-voltage connector specialty grades (USCAR-2 Class 3 hydrolysis-resistant PBT). Control-unit FR PBT (WFC061I). Halogen-free FR PA66 for premium EV programs. PA6 flame-retardant for battery housings is the next-step substitution target, not yet at parity. |

Free market intelligence for polymer distributors.