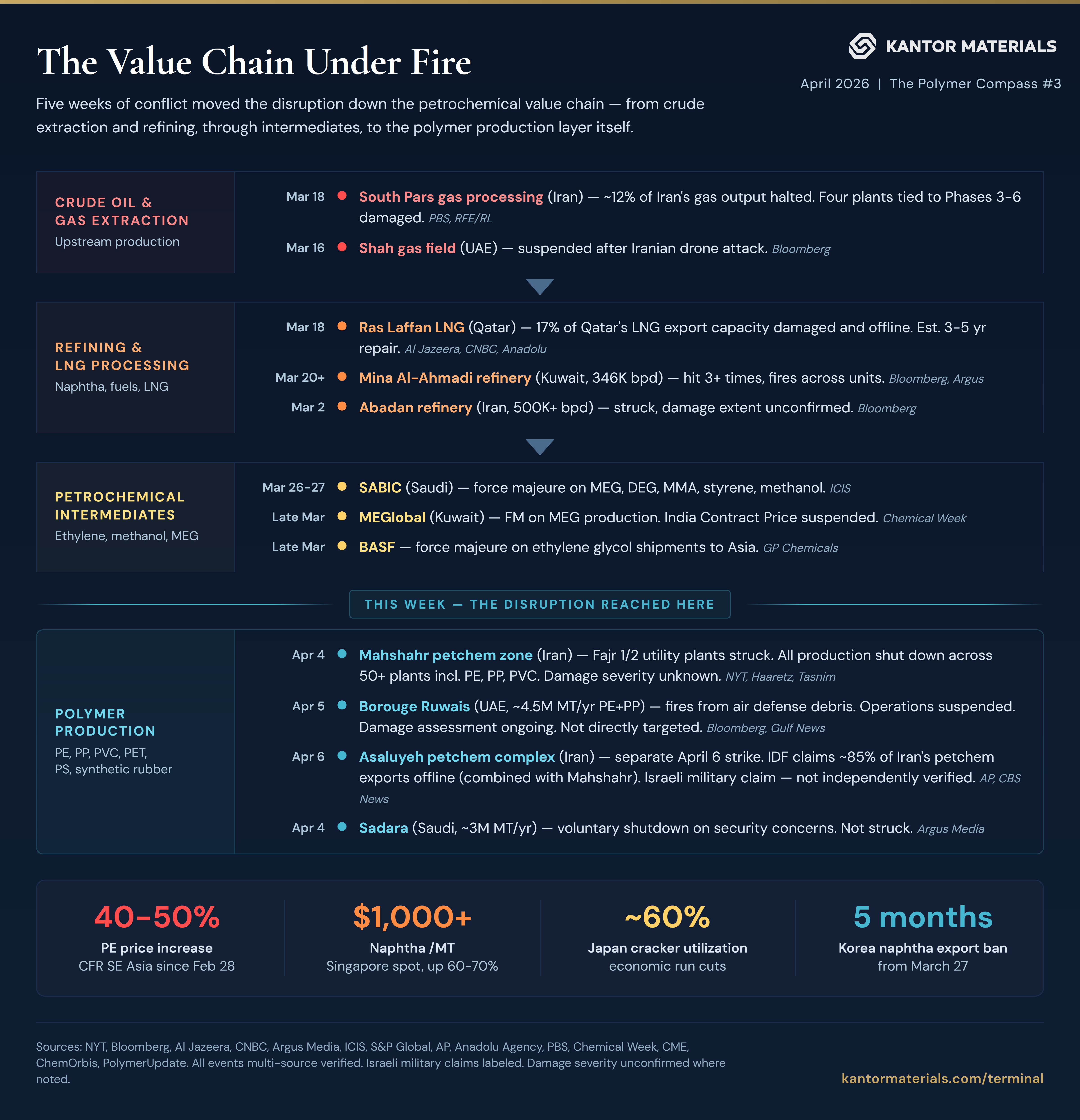

When the War Hit the Plants

Since mid-March, the conflict has been hitting energy infrastructure — refineries, LNG trains, gas processing facilities, oil fields. In the past few days, the impact moved down the value chain and reached the polymer production layer directly. A petrochemical zone's utility backbone was struck, shutting down polymer plants that depend on it. One of the world's largest single-site polyolefin facilities was suspended after debris from air defense operations caused fires on-site.

The supply disruption is no longer upstream. It is at the production line.

What follows is what can be verified, what cannot, and what the confirmed facts tell us.

1. What We Know

Iran — two petrochemical hubs struck in three days.

On April 4, US-Israeli strikes hit the Mahshahr Special Petrochemical Economic Zone in Khuzestan. The strikes targeted Fajr 1 and Fajr 2 — the utility plants that supply gas, power, and industrial water to over 50 downstream plants in the zone, including polyethylene, polypropylene, and PVC production. Rejal and Amir Kabir petrochemical facilities were also struck. Five workers were killed, approximately 170 wounded. All production across the complex was shut down, according to the New York Times citing two senior Iranian oil ministry officials.

On April 6, the IDF struck Asaluyeh — the South Pars petrochemical complex and Iran's other major petrochemical hub. This followed an earlier March 18 strike on South Pars gas processing that halted approximately 12% of Iran's gas output. Israeli Defense Minister Katz stated the two hubs combined represent approximately 85% of Iran's petrochemical export capacity, and both are "taken out of use and not functioning."

The US government has asked commercial satellite providers to withhold imagery from the conflict zone indefinitely, making independent damage verification currently impossible.

UAE — collateral damage shut one of the world's largest polyolefin sites.

On April 5, an Iranian barrage of 23 ballistic missiles and 56 UAVs targeted the UAE. Air defense systems intercepted the incoming projectiles, but falling debris struck the Borouge complex at Ruwais, sparking three fires. Operations were immediately suspended. No casualties were reported. Borouge Ruwais produces approximately 4.5 million tonnes per year of polyethylene and polypropylene. Its newest expansion, Borouge 4, had begun commercial production just days earlier.

Saudi Arabia — voluntary shutdown on security concerns.

Sadara Chemical Company, a Dow-Aramco joint venture at Jubail producing approximately 3 million tonnes per year of chemicals and plastics including PE and PP, voluntarily shut down production due to security concerns. The facility was not struck.

Confirmed market data. Naphtha has breached $1,000/MT in Singapore — up 60-70% from pre-crisis levels. PE prices are up 40-50% across Southeast Asian markets since February 28. SABIC, MEGlobal, and BASF have all declared force majeure on ethylene glycol — a critical feedstock for PET resin production.

2. What We Don't Know

Mahshahr damage severity. The utility plants were struck and all production shut down — but struck is not destroyed. The shutdown could reflect physical destruction, precautionary measures, or both. Israeli-sourced estimates cite approximately two years for reconstruction. Iran has not published a damage assessment. The absence of "minor damage" messaging from Tehran is notable but not conclusive.

Borouge damage severity. Fires have been contained. Damage assessment is ongoing. One source reports cracker unit damage; another says no major structural damage. These directly contradict. No force majeure has been formally declared. No restart timeline has been published. The difference between restart in days and repair in months is substantial — and it is not yet known which applies.

Asaluyeh specifics. The IDF claims the complex is non-functional. Which specific units were hit — ethylene crackers, methanol production, aromatics — is unconfirmed. The 85% export capacity claim is an Israeli military statement, not an independent assessment.

The April 8 deadline. Trump has set Tuesday 8 PM Eastern as the deadline for power grid and bridge strikes on Iran — the fourth deadline in a series. Iran has explicitly rejected it. A 45-day ceasefire proposal is under discussion with what White House sources describe as slim near-term odds.

3. What the Verified Facts Tell Us

Displaced demand enters the spot market.

Iran exports polymer to roughly 60 countries, with major volumes flowing to Turkey, India, and China. If Iranian supply is offline — whether partially or fully — those buyers do not stop needing material. They redirect to the global spot market, seeking replacement tonnes from the same available supply pool that serves Southeast Asian markets. Simultaneously, Borouge's customers are sourcing alternatives before the damage assessment concludes — standard procurement behavior when a major supplier's status is uncertain. Two demand waves are converging on an already constrained spot market from different directions. The supply loss is one side of the equation. The demand redirection from displaced buyers is the other.

Northeast Asian cracker restructuring extends.

South Korea's four Yeosu naphtha crackers are merging into a single entity. Japan's crackers are operating at approximately 60% capacity. Korea has banned naphtha exports for five months. These decisions predate this weekend — they were driven by naphtha at $1,000/MT and five weeks of Hormuz closure. The question of whether they reverse depends on whether naphtha economics normalize. Each escalation pushes that normalization further out. At some point, the financial and operational commitments of Korea's cracker consolidation become cheaper to complete than to unwind. That threshold is measured in months.

The PET feedstock chain is under simultaneous pressure.

Three major producers of ethylene glycol — a key raw material for PET resin, used in packaging, bottles, and polyester fiber — have declared force majeure: SABIC (Saudi Arabia), MEGlobal (Kuwait), and BASF. If ethylene glycol supply stays tight, PET resin costs rise. How long prices stay elevated depends on how quickly producers outside the Middle East can make up the production shortfall.

4. What to Watch

- Tuesday April 8th, 8:00PM EST — power grid and bridge strike deadline. Fourth deadline in the series. Same extension pattern, or different.

- Borouge damage assessment — determines whether 4.5 million tonnes per year is offline for days or months.

- Insurance and freight repricing — war risk premiums are being recalculated to include facility risk alongside transit risk. Container reallocation from the dual Hormuz and Red Sea disruption is tightening vessel availability on routes that do not transit either chokepoint. The combined landed cost impact is emerging but not yet quantifiable.

- Monday market open — Brent and DCE futures will price this weekend's developments. First hard data since Thursday.

Related

If you source from Mahshahr, Asaluyeh, Borouge, or Sadara, the Hormuz polymer substitution guide maps these producers' most common grades to Chinese, Korean, and Thai alternatives — with COA parameter tables and landed-cost calculations for Ho Chi Minh City, Jakarta, Istanbul, and Delhi buyers.

Free market intelligence for polymer distributors.