The Co-Product Problem: Why PP Got Hit Harder Than PE

When a cracker shuts down, it doesn't just stop making polyethylene. It stops making the feedstock for five polymer families simultaneously.

This Week's Number

60% of ethylene becomes polyethylene. The other 40% feeds a range of industrial chemicals — and, critically for polymer buyers, the feedstock chains for PVC, PET, and polystyrene. Every cracker shutdown is not one shortage. It is several, simultaneously.

1. The Headline Understates the Disruption

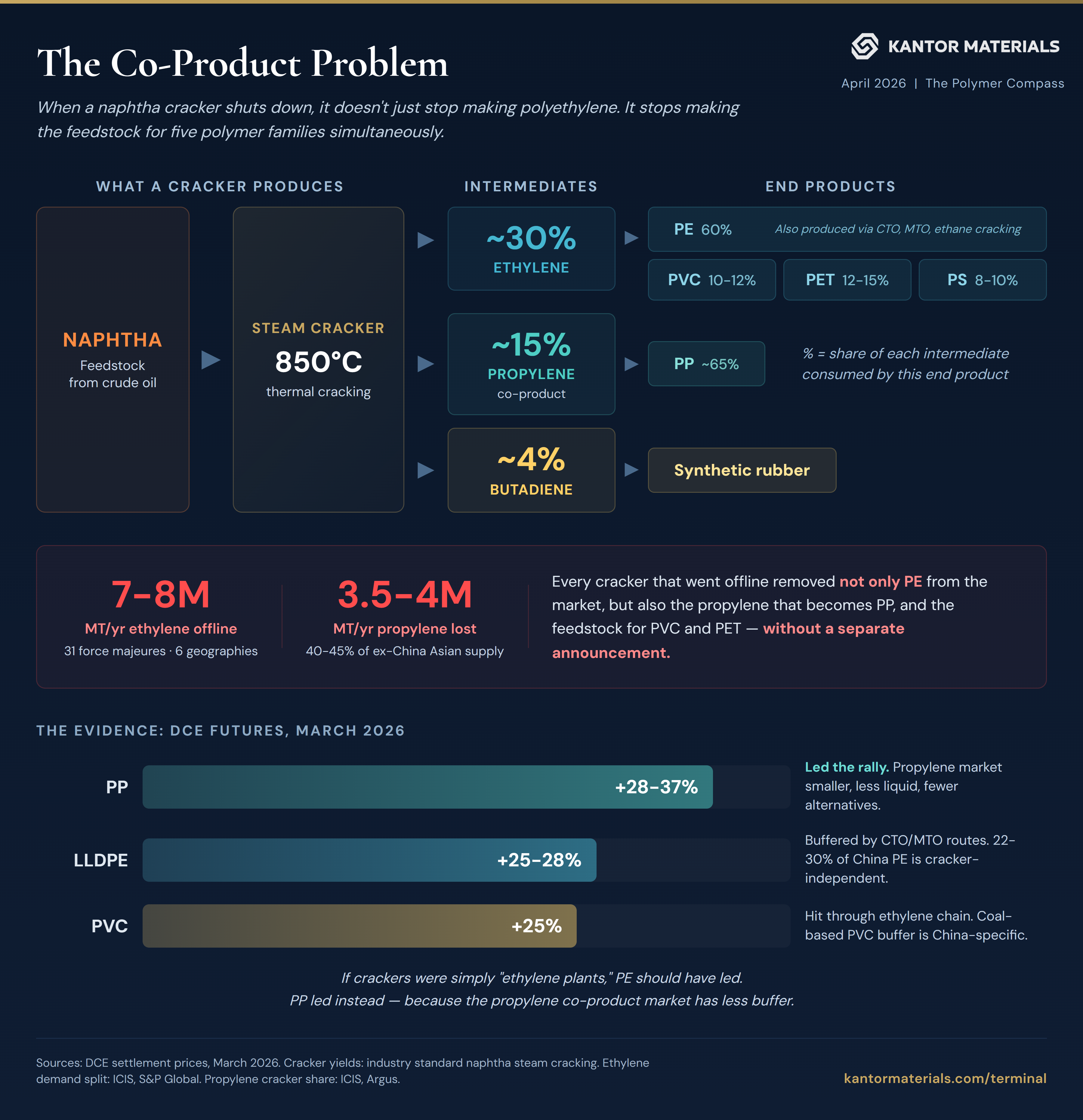

Thirty-one force majeure declarations across six Asian producing geographies. An estimated 7-8 million tonnes per year of ethylene capacity offline. These are the numbers that have defined the Hormuz crisis for polymer markets since late February.

But ethylene capacity is not the full picture. It may not even be the most important part of it.

A naphtha steam cracker does not produce ethylene alone. It produces multiple outputs simultaneously — and when it shuts down, all of them stop. The disruption to polyethylene supply is visible because crackers are commonly described as "ethylene plants." The disruption to polypropylene, PVC, PET, and polystyrene supply is less visible — but in some cases, more severe.

2. What a Cracker Actually Produces

When naphtha enters a steam cracker at approximately 850 degrees Celsius, it breaks into a portfolio of products. Not one output. Several, in fixed proportions determined by chemistry:

- Ethylene — ~30% of output by weight

- Propylene — ~15%

- Butadiene — ~4%

- Pyrolysis gasoline, methane, hydrogen: remainder

Ethylene is the primary product. Roughly 60% of it becomes polyethylene. But the remaining 40% feeds other polymer chains entirely: 10-12% becomes the feedstock for PVC (via ethylene dichloride and vinyl chloride monomer), 12-15% becomes the feedstock for PET (via ethylene oxide and monoethylene glycol), and 8-10% feeds polystyrene production.

Propylene is the co-product. It receives less attention, but it matters enormously: approximately 65% of propylene becomes polypropylene. And in Asia outside China, steam crackers supply 40-45% of all propylene. There is no other source at comparable scale.

This means the 7-8 million tonnes of offline ethylene capacity simultaneously removes an estimated 3.5-4 million tonnes per year of propylene from the market. Every cracker that declared force majeure removed not only its polyethylene output from the market, but also — without a separate announcement — its propylene, butadiene, and the upstream feedstock for PVC and PET.

3. Which Polymer Families Got Hit Hardest

If crackers were simply "ethylene plants," polyethylene should have led the March price rally. It did not.

- PP: +28-37% (DCE futures, March 2026)

- LLDPE: +25-28%

- PVC: +25%

Polypropylene moved the most — and by a meaningful margin.

The reason is structural. Ethylene has more flexible supply sources than propylene does. In China, 22-30% of polyethylene production capacity runs on coal-to-olefins and methanol-to-olefins pathways that have zero connection to naphtha crackers. These kept running and kept producing through the entire crisis. Ethylene also has a deeper, more liquid global spot market and, in the Middle East and United States, ethane-based crackers that operate on entirely different feedstock.

Propylene has no equivalent buffer — at least not outside China. When naphtha crackers shut down in Korea, Taiwan, Thailand, and Indonesia, the production base that supplies 40-45% of the region's propylene was severely impaired. The propylene market is smaller, less liquid, and had less inventory depth to absorb the shock. The result: PP prices moved faster and further than PE prices, despite the fact that no polypropylene plant declared force majeure.

The connection between ethylene cracker shutdowns and PP supply tightening is well understood at a general level — when major production centers go offline, everything tightens. What the co-product mechanism makes precise is why PP moved further than PE despite being the secondary output: the propylene market is structurally less buffered. Fewer alternative routes, less liquidity, less inventory depth. The same upstream shock produced a larger downstream price response in propylene than in ethylene — and the March DCE data reflects exactly that.

The corollary applies across families. These are not four independent shortages. They are one shortage — naphtha cracker capacity — expressing itself across multiple polymer families through a shared upstream constraint. A single cracker restart relieves PE, PP, PVC feedstock, and PET feedstock simultaneously. A single new shutdown tightens all of them. For buyers who source across polymer families, supply risks that appear diversified are in fact correlated through the cracker.

4. Kantor Indicative Pricing

As of April 3, 2026 | China-origin | CFR Ho Chi Minh City:

- PP Yarn (T30S): $1,263/MT

- PP Injection: $1,273/MT

- PP Fiber (Y16): $1,335/MT

- LLDPE 7042 (C4): $1,263/MT

- HDPE Film (7260): $1,158/MT

All prices Kantor Indicative. This is our first full-grade pricing table — covering PP, PE, and HDPE from China-origin production. Week-on-week comparisons begin next issue.

Market conditions:

- Availability: TIGHT — 31 force majeures, six geographies offline. No restart dates announced.

- Price: RISING — Brent above $110. Naphtha economics remain unviable for most idled crackers.

- Supply window: NARROWING — operating capacity is finite. Each week without cracker restarts draws regional inventory lower.

How to read this: If you source both PE and PP, your supply risks are not independent — they are connected through the cracker co-product mechanism described above. Tightening in one family signals tightening in the other. Monitor your combined exposure, not each grade in isolation.

5. What This Means Going Forward

The co-product mechanism is not a crisis artifact. It is how naphtha-based petrochemical production has always worked. The crisis has made it visible by shutting down enough cracker capacity simultaneously to move prices across multiple polymer families at once — but the underlying structure is permanent.

Two observations worth carrying forward:

First, the severity of impact across polymer families is not proportional to the size of each market. It is proportional to the availability of alternative supply routes. Polyethylene has coal-to-olefins and ethane-based alternatives. Polypropylene, outside China, largely does not. The polymer with the fewest alternative production pathways absorbs the largest price impact from a shared upstream disruption — regardless of whether it is the cracker's primary product or its co-product.

Second, supply diversification across grades does not equal supply diversification across risk. A buyer purchasing PE from one supplier and PP from another may believe their supply chain is diversified. If both suppliers source from naphtha crackers, the risk is the same risk — expressed through two different product names.

Understanding which of your polymers share upstream dependencies is the first step toward procurement that accounts for the actual structure of supply, not just the labels on the product.

Related

The structural reason China's CTO (coal-to-olefins) and PDH (propane dehydrogenation) producers are insulated from naphtha-driven co-product cascades is explained in the CTO, PDH, and naphtha feedstock economics guide. These alternative routes decouple ethylene and propylene from each other — which is why Chinese PE and PP continued quoting into tight markets while naphtha-cracker PP rallied hardest.

Free market intelligence for polymer distributors.